Nigeria’s 2025 decision to raise the minimum capital base for insurance companies is long overdue — and undeniably important.

It signals stronger regulatory intent, renewed protection for shareholders and policyholders, and recognition that Nigeria’s insurance industry cannot remain undercapitalised in a high-risk, fast-growing economy.

But here’s the hard truth:

The reform fixes yesterday’s weaknesses more than tomorrow’s challenges.

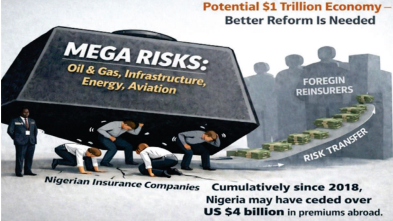

The Bigger Problem: Premiums Flowing Overseas

Behind the recapitalisation headlines lies a structural imbalance that continues to drain the economy.

Foreign reinsurers dominate an estimated 65% of Nigeria’s reinsurance market, especially in high-value sectors such as:

- Oil and gas

- Aviation

- Infrastructure

- Energy

Because many local insurers lack the capital to underwrite large risks, billions of naira in premiums are ceded abroad each year.

The consequences are significant:

- Pressure on foreign exchange

- Reduced domestic investment capacity

- Limited role for insurers in financing national development

The 2025 reform may improve capacity marginally — but most Nigerian insurers still cannot retain major risks without heavy foreign support.

And that means the premium leakage continues.

A Capital Market Opportunity Nigeria Is Missing

Insurance companies are not just risk managers. They are natural long-term investors.

Globally, insurers are pillars of capital markets. They provide liquidity, support infrastructure financing, and strengthen corporate governance.

Yet Nigeria’s insurance presence on the Nigerian Exchange (NGX) remains limited.

Major players such as:

- Leadway Assurance

- Zenith General Insurance

could significantly deepen the market through public listings.

Listing would:

- Expand investor access to the sector

- Improve transparency

- Retain more premiums domestically

- Mobilise long-term capital for infrastructure

At a time when Nigeria urgently needs patient capital, the insurance sector remains under-leveraged.

Lessons from 2007: Reform Works — When It’s Bold

Nigeria has been here before.

The 2007 recapitalisation exercise — combined with the “No Premium, No Cover” policy — reshaped the industry. It:

- Attracted banking-sector investment

- Forced weak firms out

- Encouraged consolidation

- Improved underwriting discipline

The key lesson?

Capital adequacy matters.

But even after the 2025 exercise, Nigerian insurers remain small compared to peers in emerging and developed markets — where firms can:

- Underwrite mega infrastructure projects

- Absorb catastrophic losses

- Invest in actuarial science and advanced risk modelling

- Compete across borders

Nigeria’s insurers, by contrast, still rely heavily on foreign reinsurers for large-ticket risks.

The result: premium leakage, FX strain, and diminished economic sovereignty.

Bigger Balance Sheets Are Not Enough

Recapitalisation alone does not guarantee competitiveness.

Nigeria still has too many insurers chasing limited business. Consolidation may reduce numbers, but size without capability solves little.

Structural gaps remain in:

- Corporate governance

- Risk management systems

- Actuarial expertise

- Product innovation

- Distribution channels

- Digital infrastructure

The planned transition to a Risk-Based Capital (RBC) framework is a positive move. But RBC systems are data-heavy, complex, and costly — and they cannot compensate for poor pricing or weak supervision.

Without deeper reform, insurers may become larger on paper but not stronger in practice.

Insurance and Nigeria’s Growth Ambition

Insurance penetration in Nigeria remains between 0.5% and 1% of GDP — far below the 5–10% typical of mature markets.

For a country targeting a $1 trillion economy, this gap is more than symbolic.

A strong domestic insurance sector would:

- Retain premiums locally

- Strengthen resilience of public assets

- Finance long-term infrastructure

- Deepen participation in the NGX

- Reduce FX pressure

Right now, Nigeria insures its biggest risks abroad.

That is neither sustainable nor strategic.

What Policymakers Must Do Next

If Nigeria is serious about building a globally competitive insurance ecosystem, the next steps must go beyond recapitalisation.

1. Raise capital thresholds further — especially for reinsurers

High-risk sectors like oil and gas may require dollar-linked capital requirements to reflect FX exposure and global standards.

2. Align capital more closely with actual risk exposure

Insurers should be able to retain a larger share of domestic risks.

3. Encourage major insurers to list on the NGX

Transparency and market participation would strengthen both the industry and capital markets.

4. Create government-backed insurance schemes

Critical infrastructure and public-sector risks could provide predictable demand and strengthen local balance sheets.

5. Establish a National Strategic Risk Pool

Potentially funded through infrastructure insurance bonds, such a vehicle could reduce dependence on offshore markets.

6. Strengthen governance and regulatory consistency

Reforms must be insulated from policy reversals and weak enforcement.

The Strategic Choice

The 2025 recapitalisation reform is progress.

But progress is not transformation.

Without scale, capability, and meaningful risk retention, Nigeria’s insurance sector will continue exporting premiums, profits, and influence abroad.

A $1 trillion economy cannot rely on foreign markets to insure its most valuable assets.

Nigeria must decide:

Build insurers strong enough to underwrite national risks at home — or continue sending billions overseas.

The window for decisive reform is open. The question is whether policymakers will go far enough this time.