Chartered Insurance Institute of Nigeria (CIIN) has issued a strong call to insurance operators: strengthen financial controls, tighten governance, and reinforce compliance — or risk falling behind in a tougher 2026 business environment.

Speaking at the Institute’s 2026 Business Outlook in Lagos, CIIN President/Chairman, Yetunde Ilori, warned that the industry must stop treating governance as a regulatory checkbox and start seeing it as a strategic necessity.

Governance Is No Longer Optional

Held at Paradise Event Arena in Yaba, the forum — themed “Navigating Complexity: Strengthening Financial Controls, Corporate Governance and Compliance in the Insurance Industry” — gathered regulators, CEOs, board members, and senior stakeholders.

Ilori described today’s operating climate as defined by:

- Rapid economic shifts

- Evolving regulations

- Digital transformation

- Heightened stakeholder expectations

“The insurance industry today operates in an environment of increasing complexity,” she said. “For our industry to remain resilient and trustworthy, we must continuously strengthen internal controls, promote transparency, uphold ethical leadership and align strictly with regulatory requirements.”

Her message was clear: controls and governance are not administrative burdens — they are survival tools.

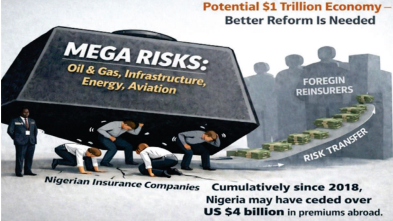

Nigeria’s Insurance Gap: A Stark Reality

The keynote speaker, Oluwatoyin Sanni, Executive Vice-Chair of Emerging Africa Group, delivered a sobering assessment of the sector’s structural weaknesses.

Globally, insurance contributes 6–7% of GDP.

In Nigeria? Less than 1% penetration.

For context:

- South Africa: approximately 14%

- Kenya: about 2.3%

“Insurance penetration is not just an industry metric,” Sanni noted. “It is a measure of economic resilience, capital depth and institutional trust.”

Despite having over 50 licensed insurers and gross written premiums exceeding ₦1 trillion, Nigeria’s insurance contribution to GDP remains disproportionately low.

The Trust Deficit and Structural Weaknesses

Sanni identified key obstacles holding the industry back:

- Persistent public distrust, especially around claims settlement

- Weak financial discipline

- Fragmented balance sheets

- Undercapitalisation

- Poor alignment between cash flows and claims projections

- Inadequate technical reserves

She warned that weak internal controls and manual processes are amplifying operational risks — particularly in a volatile macroeconomic environment.

At the heart of these challenges, she said, lies one issue:

Financial control is the first line of survival during economic stress.

2026 Budget Signals Tougher Conditions

Sanni linked her analysis to the Federal Government’s 2026 Budget, themed “Consolidation, Renewed Resilience and Shared Prosperity.”

According to her, the fiscal direction points to:

- Tighter liquidity conditions

- Inflationary pressure

- Stricter regulatory oversight

Insurers, she argued, must proactively:

- Strengthen capital planning

- Optimise reinsurance structures

- Build adequate reserves to absorb shocks

Boards Must Step Up

Perhaps her strongest message was directed at boards of directors.

Boards, she said, must move beyond passive oversight and actively engage in:

- Underwriting standards

- Investment strategy

- Capital adequacy decisions

- Operational risk management

“Boards must clearly define and own the firm’s risk appetite, demand early warning indicators — not post-mortem reports — and ensure the independence of risk, audit and compliance functions,” she stressed.

She also warned against treating IFRS 17 implementation as a mere compliance exercise, urging insurers to embrace it as a shift toward risk-sensitive, economic-value reporting.

Governance as Competitive Advantage

On corporate governance, Sanni was unequivocal:

“Weak governance destroys trust faster than poor financial performance.”

She urged insurers to:

- Align executive pay with risk-adjusted performance

- Embed ethical leadership

- Strengthen board committees with skilled and independent members

Rather than viewing governance as a regulatory burden, she described it as a potential competitive advantage in rebuilding public confidence.

The Bottom Line

As 2026 approaches, Nigeria’s insurance industry faces a tightening operating climate shaped by economic pressure and rising regulatory expectations.

CIIN’s message is unmistakable:

- Strengthen financial controls.

- Reinforce governance structures.

- Build trust.

In a sector where credibility is currency, insurers that fail to adapt may struggle to survive the complexity ahead.